|

| Image source |

I'll borrow a quip from John Rust here. In Lewis Carroll's famous tale. Alice reacts to hearing the poem Jabberwocky:

Somehow it seems to fill my head with ideas--only I don't exactly know what they are.That's how I feel when I hear people talk about "the fiscal multiplier." The fiscal multiplier isn't a thing. It's not a structural parameter governing economies that we just need to discover. The response of the economy to government spending is likely to depend heavily on the state of the economy and the nature of the spending (definitely read that last link, and read this one too).

This is true of a lot of useful "reduced-form" relationship estimates, of course, but in my mind the fiscal multiplier is the king of reduced-form-ness. The outcome being measured is too far downstream from the treatment causing that outcome--and this is saying nothing of the even more relevant fact that under the usual monetary policy objectives, the "fiscal multiplier" might only be an estimate of the central bank's incompetence.

I know the fiscal multiplier is reasonably well defined in New Keynesian and related models. But it's not easy for me to map that concept onto the real world (while, believe it or not, I can do so with a lot of other NK concepts).

I'm not suggesting that estimating fiscal multipliers is a waste of time or that the estimates we do have are useless. By all means, let's keep researching the range of effects of fiscal policy. I'm just suggesting that the meaning of the multiplier is not always clear, and cherry picking multiplier estimates from the literature to support one's preferences is probably disingenuous. More generally, nobody will ever convince me of the necessity of fiscal stimulus (or of avoiding "austerity") by citing a few multiplier estimates.

Jeffrey Sachs bemoans the prevalence of "crude Keynesianism" in the national policy debate, where crude Keynesians embraces the following:

(1) The belief that multipliers on tax cuts and transfers are stable, predictable and large;I don't mean to take a stand on the causes of our prolonged employment problems. I had strong views on that back in the days before I realized how confused I am, but not anymore. Even so, I can't think of any reason to believe that good policy can be based on such a temperamental idea as the fiscal multiplier.

(2) The belief that America's employment and growth problems are overwhelmingly cyclical, not structural, and therefore remediable by short-term aggregate demand management;

(3) The belief that a growing debt burden is a minor nuisance as long as the economy is in recession;

(4) The belief that for practical purposes, the most urgent need is to raise aggregate demand rather than to focus on the quality and type of public spending.

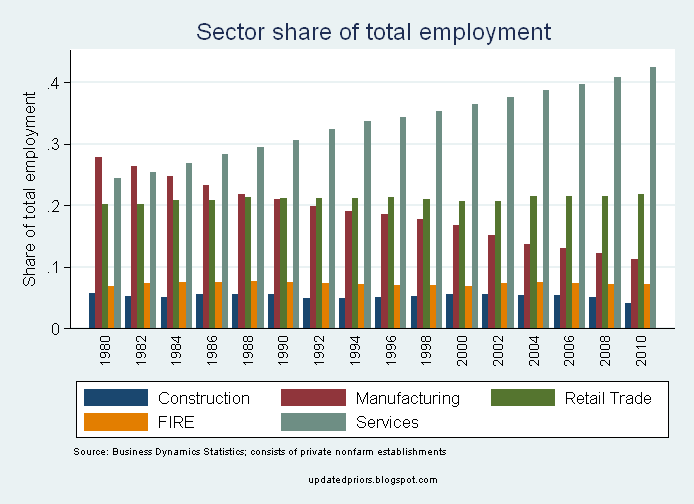

I also have no serious position on the related issue of structural vs. cyclical elements of the employment problem. While inflation and inflation expectations stay low, I'm not going to be too concerned about having too much demand stimulus. I know about papers like this one. But I would also say that given some of the secular trends we see in the U.S. economy, it's pretty hard to believe that structural forces are not playing any role in this business cycle. Some data from this post (click for larger images):

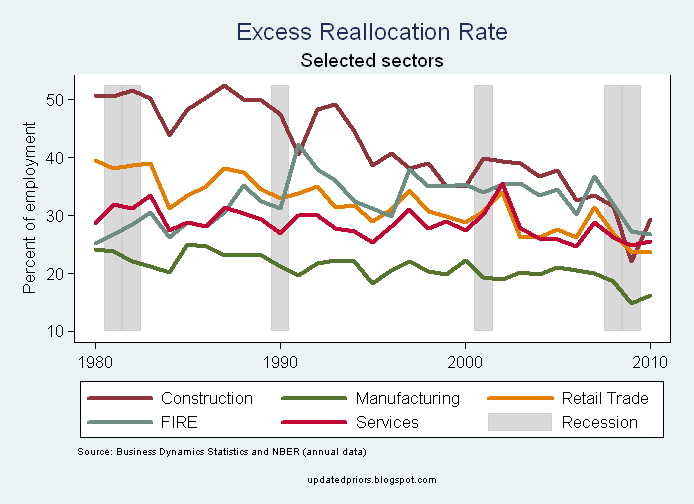

And here's one from this post:

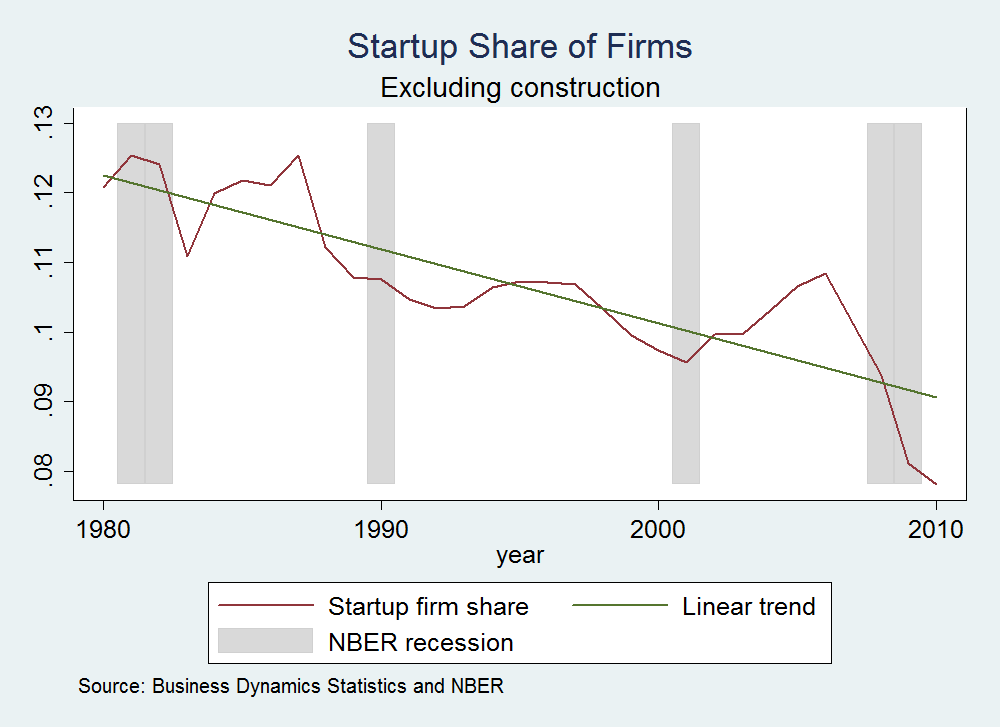

...which should be considered along with one from this post:

There are clearly some big secular trends in the structure of the U.S. economy. Something has been going on for the last 30 years or so. The degree to which this secular stuff affects the business cycle, and the effect that fiscal policy might have on it all, depend on what is causing all these changes. We have a good idea about some of it, but we don't fully understand it all. I think some caution and intellectual humility are appropriate when we make claims about what's going on and what policies we should be applying.