Timothy B. Lee has a new interview with Marc Andreessen (h/t Tyler Cowen) about "the death of the IPO." An excerpt:

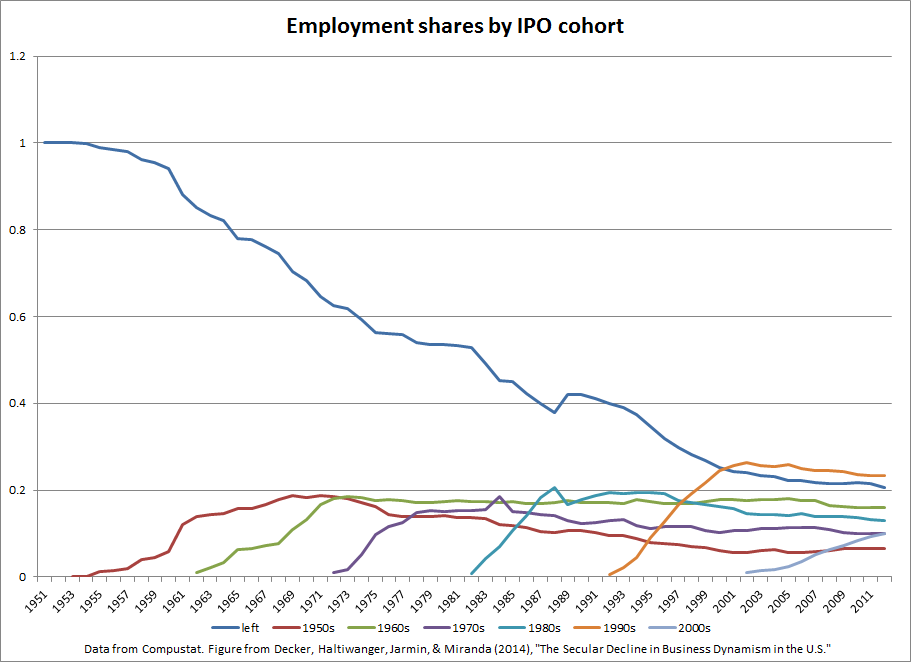

So the argument is that high-growth firms now do their serious growth prior to going public. In a new working paper (with coauthors, discussed here and here), we find some evidence consistent with this idea. Here's Figure 15 from our paper:

![]()

Here we've sliced the Compustat data by IPO cohort, with cohorts defined by a decade. The lines show each cohort's share of total employment (among publicly traded firms). So, for example, the red line shows that the cohort of firms that went public in the 1950s rose to almost 20 percent of employment by 1970 and has gradually declined ever since.

The 1970s, 1980s, and 1990s cohorts gained employment share rapidly, with the explosive 1990s IPOs actually becoming the largest cohort by around 2000. But the 2000s cohort is a bit of a dud. It only gains employment share very gradually; and, unlike previous cohorts, after 10 years it is still a long way from being a large cohort.* And by the way: if you do this by sales instead of employment it looks pretty much the same (not shown in the paper). The figure alone isn't a smoking gun, but it's suggestive; and other evidence in our paper demonstrates that the growth distribution for public firms has tightened and unskewed since ~2000 (e.g., Figure 14).

You could probably tell a few stories for why the 2000s cohort looks so different. One of them could be Andreessen's. I don't know anything about that stuff so I won't comment.

But the patterns are pretty striking.

*We also show in the paper (see Figure 16) that the 1980s and 1990s cohorts were more volatile than both the cohorts that preceded them and the 2000s cohort, a composition effect which helps explain the aggregate trend I discussed in my last post; see also Davis, et al. (2007)![]()

There's been an absolutely dramatic change. What you say is exactly right. Twenty years ago, IPOs had gotten democratized. You had Microsoft able to go public at less than $1 billion valuation. If you invested in Microsoft's IPO and held you had the prospect in the public market of a 1,000-times gain. There were a whole bunch of other comparable situations over the years. With Oracle, most of the gain was in the public market. In prior eras, the same was true of IBM and Hewlett Packard. These companies primarily grew up in the public market. . . .

The result of all that is the effective death of the IPO. The number of public companies in the US has dropped dramatically. And then correspondingly, growth companies go public much later. Microsoft went out at under $1 billion, Facebook went out at $80 billion. Gains from the growth accrue to the private investor, not the public investor.

So the argument is that high-growth firms now do their serious growth prior to going public. In a new working paper (with coauthors, discussed here and here), we find some evidence consistent with this idea. Here's Figure 15 from our paper:

The 1970s, 1980s, and 1990s cohorts gained employment share rapidly, with the explosive 1990s IPOs actually becoming the largest cohort by around 2000. But the 2000s cohort is a bit of a dud. It only gains employment share very gradually; and, unlike previous cohorts, after 10 years it is still a long way from being a large cohort.* And by the way: if you do this by sales instead of employment it looks pretty much the same (not shown in the paper). The figure alone isn't a smoking gun, but it's suggestive; and other evidence in our paper demonstrates that the growth distribution for public firms has tightened and unskewed since ~2000 (e.g., Figure 14).

You could probably tell a few stories for why the 2000s cohort looks so different. One of them could be Andreessen's. I don't know anything about that stuff so I won't comment.

But the patterns are pretty striking.

*We also show in the paper (see Figure 16) that the 1980s and 1990s cohorts were more volatile than both the cohorts that preceded them and the 2000s cohort, a composition effect which helps explain the aggregate trend I discussed in my last post; see also Davis, et al. (2007)