About a decade ago, people were looking at Compustat data (which provide financial statement information for public firms) and noticing that various measures of employment and sales volatility appeared to be on an upward secular trend. They were casting about, looking for a explanation for why US firms were becoming more volatile. More volatile productivity shocks? A composition shift to industries that were naturally more volatile? Globalization? That sort of thing.

In 2006, Davis, et al. showed that the increasing volatility trend was actually unique to public firms (that paper also cites the studies that originally found and explored the trend among public firms). Once you look at the entire universe of US firms, public and private, you see an opposite trend, one that I've discussed many times and done some research on with coauthors: declining volatility. So the mystery was actually: why are public firms becoming more volatile while private firms are becoming less volatile?

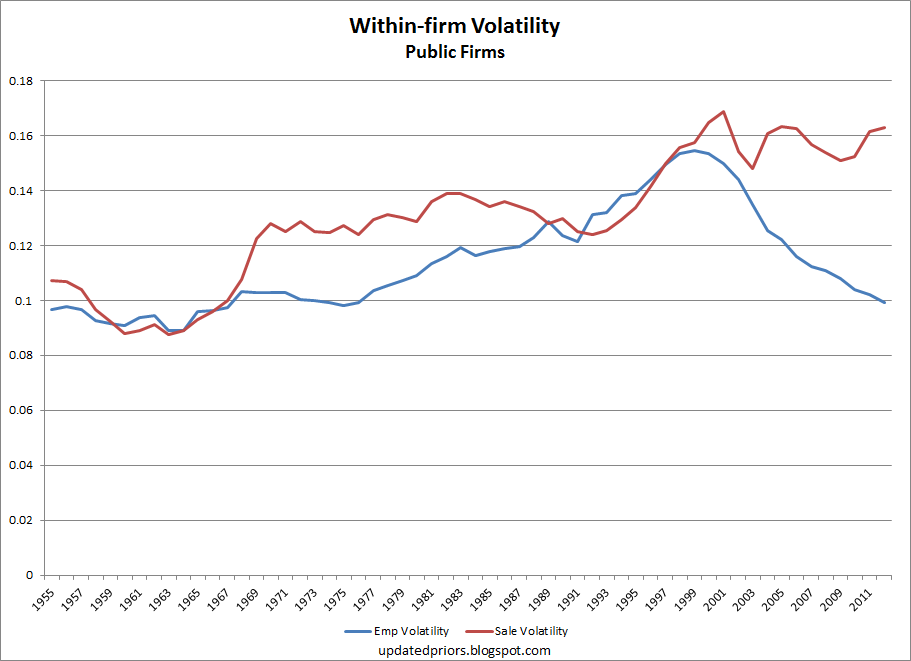

Fast forward to today. In a new working paper (preliminary and incomplete), coauthors and I show that the trend of increasing volatility among public firms appears to have reversed. Here are data from Compustat*:

Employment volatility shows a pretty clear reversal starting in the early 2000s, while sales volatility appears to level off. However, sales variables are very sensitive to, e.g., industry-specific prices and other stuff, and we show in the paper that if industry effects are removed sales volatility also declines in the post-2000 period. To my knowledge, this trend reversal among public firms is a new fact. Some readers might also find the relationship between sales and employment volatility over time interesting.

![]()

In 2006, Davis, et al. showed that the increasing volatility trend was actually unique to public firms (that paper also cites the studies that originally found and explored the trend among public firms). Once you look at the entire universe of US firms, public and private, you see an opposite trend, one that I've discussed many times and done some research on with coauthors: declining volatility. So the mystery was actually: why are public firms becoming more volatile while private firms are becoming less volatile?

Fast forward to today. In a new working paper (preliminary and incomplete), coauthors and I show that the trend of increasing volatility among public firms appears to have reversed. Here are data from Compustat*:

|

| Compustat data (non-confidential) Click for larger image |

So we can add publicly traded firms to the list of business types that are experiencing declining churn and volatility.

*The volatility measure used here is the "modified Comin" measure discussed in Davis, et al. (2006). Basically think of the standard deviation of a firm's growth rates over a 10-year period, but modified to better use endpoints. The aggregate measure is just an activity-weighted average of the firm measures.