On this blog, I've been trying to describe what's going on in the US economy. This entails looking at two things: long-term secular trends and cyclical issues. Before you stop reading, just note that a lot of the current US policy debate relates to questions about whether our current problems are structural or cyclical. I'll have some comments on that at the end of this post (you can skip to that if you want).

The BED* provides data on job creation from entering, exiting, expanding, and contracting establishments.** Readers of this blog already know that entry is pretty important, since startups typically account for all net job creation. The rich BED data provide insights into the related issue of establishment dynamics.

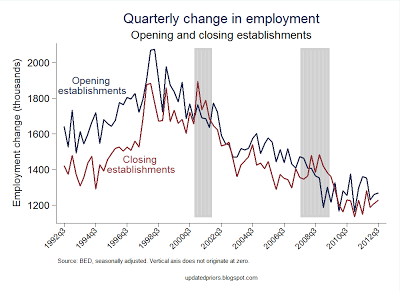

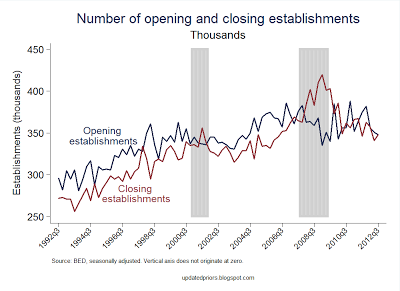

Figure 1 plots employment flows for opening and closing establishments, respectively, since 1992 (the beginning of the BED). Figure 2 plots the number of establishments that opened or closed, respectively, by quarter. In both charts, the grey bars indicate NBER recession dates. Click either chart for a larger image.

In each chart, the blue line corresponds with opening establishments, and the red line corresponds with closing establishments. Speaking very roughly, in Figure 1 you can see the net employment flow for entry/exit as the blue line minus the red line; and in Figure 2 you can see the net change in the number of business establishments as blue minus red (I say "roughly" because each series is individually seasonally adjusted, and this can lead to very rough comparisons).

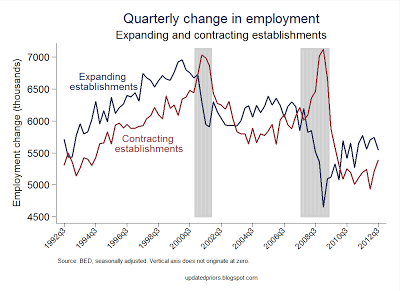

Again, blue line minus red line gives (roughly) net job creation (Figure 3) or net new establishments (Figure 4). In employment terms, the gap between growth and contraction during the 2000s is not so different from the gap during the 1990s (which is different from what we saw in entry/exit). Have net job flows recovered back to pre-Great Recession levels? Maybe. But we do see something in Figure 4: the net gap was larger in the 1990s than in the 2000s or 2010s. In Figure 3 we see a marked stair-step pattern in gross flows. It's as if the last two recessions have caused gross flows to drop to permanently lower levels without signs of linear growth or decline.

![]()

The BED* provides data on job creation from entering, exiting, expanding, and contracting establishments.** Readers of this blog already know that entry is pretty important, since startups typically account for all net job creation. The rich BED data provide insights into the related issue of establishment dynamics.

Figure 1 plots employment flows for opening and closing establishments, respectively, since 1992 (the beginning of the BED). Figure 2 plots the number of establishments that opened or closed, respectively, by quarter. In both charts, the grey bars indicate NBER recession dates. Click either chart for a larger image.

|

| Figure 1 |

|

| Figure 2 |

In each chart, the blue line corresponds with opening establishments, and the red line corresponds with closing establishments. Speaking very roughly, in Figure 1 you can see the net employment flow for entry/exit as the blue line minus the red line; and in Figure 2 you can see the net change in the number of business establishments as blue minus red (I say "roughly" because each series is individually seasonally adjusted, and this can lead to very rough comparisons).

What do you see in the figures? The downward trend in job flows-related quantities that I've described in other posts can be clearly seen on Figure 1 in the post-1998 period (and it's interesting that the peak occurred before the 2001 recession). My best guess--based on BDS data--is that the 1990s data show a temporary leveling off of the flows data in the middle of a decades-long downward trend (BED data only go back to 1992).

Also in Figure 1, observe that the gap between opening and closing establishment job flows was large in the 1990s and did not again reach that magnitude in the 2000s or 2010s. In both Figures 1 and 2, we see that the post-Great Recession period has been an extended period of the tightest entry/exit gap of the last two decades. There has been no return to a world of much more entry than exit of businesses. In the post-Great Recession world so far, entry and exit basically offset each other, including in their job market contributions. And the long-term trends in both charts have been moving sideways for several years now.

Now we'll consider existing establishments that are expanding or contracting. Figure 3 shows job flows at existing expanding and contracting establishments, respectively. Figure 4 shows the number of expanding and contracting establishments, respectively. Click either chart for a larger image.

|

| Figure 3 |

|

| Figure 4 |

Again, blue line minus red line gives (roughly) net job creation (Figure 3) or net new establishments (Figure 4). In employment terms, the gap between growth and contraction during the 2000s is not so different from the gap during the 1990s (which is different from what we saw in entry/exit). Have net job flows recovered back to pre-Great Recession levels? Maybe. But we do see something in Figure 4: the net gap was larger in the 1990s than in the 2000s or 2010s. In Figure 3 we see a marked stair-step pattern in gross flows. It's as if the last two recessions have caused gross flows to drop to permanently lower levels without signs of linear growth or decline.

Figures 3 and 4 say a lot about the Great Recession. In particular, the Great Recession involved both a massive spike in contractions and a large drop in expansions. The post-Great Recession period, though, is more about a pullback in contractions than it is a recovery in expansions. In both figures, the expansion/contraction gap closed rapidly, then moved sideways. And we have that troubling final data point (3rd quarter 2012) where expansions and contractions are almost equal; let's hope that's just temporary.

In general, the four figures show the following: Gross flows have not recovered to pre-Great Recession levels (this is not surprising from other data we've seen). Contraction of establishments has healed to low levels again, but expansion has barely recovered. Establishment entry has generally been barely enough to stay ahead of establishment exit, leaving existing expanding establishments to do all of the work of expanding the labor market. The Great Recession recovery period is worse than the 2001 recession period in this respect.

Note also that recessions are characterized by the red and blue lines flipping places (so exit or contraction exceed entry or expansion). But note that the entry/exit margin flipped later than the expansion/contraction margin going into the Great Recession (which is somewhat different from the 2001 recession). Both margins re-flipped several months after the Great Recession ended, which is consistent with total employment numbers (that bottomed in late 2009/early 2010).

Some comments on the cyclical vs. structural debate

In light of these data and others I've shown on this blog, how credible is the claim that current troubles are totally cyclical in nature? I haven't done anything causal here, of course, but secular trends are highly suggestive that something structural is going on. I don't know what it is. I'm not trying to stake a strong claim in this debate--I'm persuaded that cyclical things are still playing a large role--but I do think the evidence is complicated.

The US economy is always changing. The standard approach in macro is to separate growth questions from business cycle questions, but growth isn't the only trending variable in an economy. Other variables have been undergoing big changes in recent decades: industrial composition, worker/job search and match relationships, entry and the age composition of firms, international stuff, the regulatory environment, geographic patterns of economic activity ([1], [2]), and others.

It's not surprising, then, that this recovery doesn't look like previous ones. We can think of some of the reasons for this, but we don't have satisfactory explanations for the specific trends I've talked about here. Why is dynamism declining? As I noted here, we don't even know if it's a good thing or a bad thing. Do we really need the high (but declining) pace of job and worker reallocation we observe? Or is the US economy just a Rube Goldberg machine, engaging in a bunch of wasteful churning that we'd be better off without? If so, we should applaud the decline we're seeing. But if that reallocation is essential to productivity and growth in living standards, then we should be worried. Knowing what's driving it is crucial. There are some good ideas bouncing around out there, but nothing conclusive yet. The answer will at least have to account for entry and exit dynamics, for both establishments and firms.

My reading of the data suggests that secular trends may be interacting with cyclical forces in a toxic way, but I don't have any great ideas about precise mechanisms or causal factors.

*The BED are quarterly data provided from the BLS based on state UI data. They are released with a lag of about 8 months. Like the BDS (the dataset I usually use here), the BED basically covers the universe of private nonfarm employers; unlike the BDS, the BED is available at higher frequency and is released more quickly. BED has other drawbacks compared to the BDS, such as a more limited ability to track firms.

**An establishment is a single business location. A firm is a collection of one or more establishments. Costco is a firm; your local Costco store is an establishment. Usually on this blog I talk about firms (that includes all of my posts on startups, which are new firms). A count of entering establishments in the BED includes both establishments of startup firms and new establishments of existing firms. The two are conceptually different in many ways, but the public BED data do not allow us to disaggregate them.

*The BED are quarterly data provided from the BLS based on state UI data. They are released with a lag of about 8 months. Like the BDS (the dataset I usually use here), the BED basically covers the universe of private nonfarm employers; unlike the BDS, the BED is available at higher frequency and is released more quickly. BED has other drawbacks compared to the BDS, such as a more limited ability to track firms.

**An establishment is a single business location. A firm is a collection of one or more establishments. Costco is a firm; your local Costco store is an establishment. Usually on this blog I talk about firms (that includes all of my posts on startups, which are new firms). A count of entering establishments in the BED includes both establishments of startup firms and new establishments of existing firms. The two are conceptually different in many ways, but the public BED data do not allow us to disaggregate them.