"If Economists were Right, You Would Have a Raise by Now" is the title of an article by Peter Gosselin and Jennifer Oldham. I gather from the address bar that a previous title may have been "Your wallet isn't getting fatter as economics 101 comes unhinged."

What mistaken Econ 101 idea that economists embrace is to blame for this epic failure?

A lot of economists would be surprised to know that economists believe in the Phillips Curve (and that it's all about wages, but that's not my complaint). More broadly, on the first Friday of every month I see a flood of tweets about how puzzling it is that employment is growing while wages aren't rising (or are rising too slowly). I want $1 for every internet/press claim about Thing A violating Econ 101 when Thing A is perfectly consistent with Econ 101.

The article was published by a top economics news outlet! The Phillips Curve is a good example of what happens when you don't take economic theory seriously. The Bloomberg article is a good example of what happens when you write about what economists think without actually knowing what economists think.

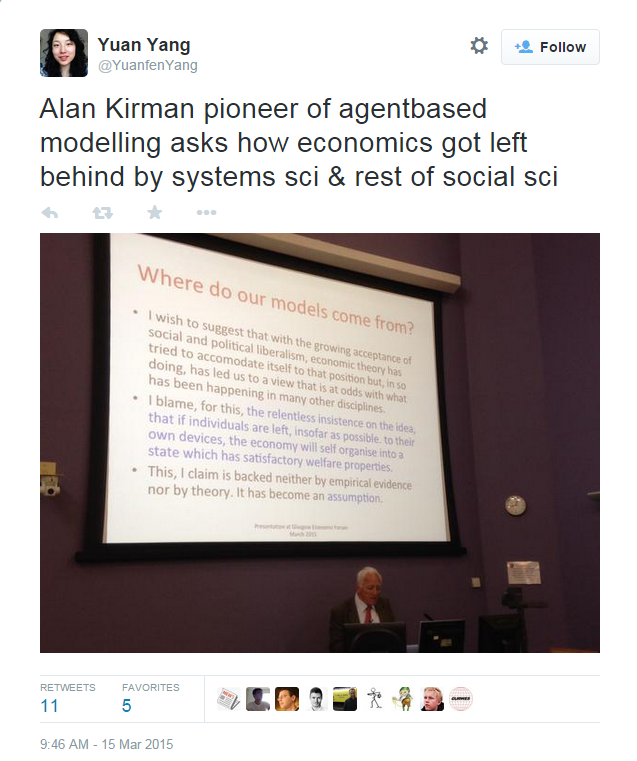

Another event this week reminded me of this odd obsession some people have with criticizing bogus caricatures of economics. Look at this tweet:

"Relentless insistence on the idea that . . . the economy will self organize into a state which has satisfactory welfare properties. . . . It has become an assumption." Anyone remotely familiar with mainstream economics knows this is, by any reasonable standard, misleading if not totally false. To the contrary, discovering and describing market failure accounts for a significant portion of economic research. Noah Smith has some nice thoughts on this.

I pointed this out to the tweeter, who responded:

Notice the sleight of hand: We started with the claim that the economics profession totally ignores market failure. When I pointed out that the claim is false, we moved to a different complaint: the Rethinkers don't like the way we study market failure. Why not say so in the first place? Click here for another example.

The sleight of hand leaves me with questions about motives. The problem with the critics of macroeconomics is not that macro is perfect as is. It's not. The problem is that they so often start with inaccurate portrayals of what people in the field actually believe and do. Progress in the discipline isn't going to be made this way. Note that this problem exists even within mainstream econ, see e.g. here and here.

Just as politics isn't about policy, perhaps demanding reforms to economics isn't about reforming economics.Image may be NSFW.

Clik here to view.

What mistaken Econ 101 idea that economists embrace is to blame for this epic failure?

One of the fundamental axioms of labor economics, called the wage Phillips curve, says that, all else equal, lower unemployment leads to higher wages.

A lot of economists would be surprised to know that economists believe in the Phillips Curve (and that it's all about wages, but that's not my complaint). More broadly, on the first Friday of every month I see a flood of tweets about how puzzling it is that employment is growing while wages aren't rising (or are rising too slowly). I want $1 for every internet/press claim about Thing A violating Econ 101 when Thing A is perfectly consistent with Econ 101.

The article was published by a top economics news outlet! The Phillips Curve is a good example of what happens when you don't take economic theory seriously. The Bloomberg article is a good example of what happens when you write about what economists think without actually knowing what economists think.

Another event this week reminded me of this odd obsession some people have with criticizing bogus caricatures of economics. Look at this tweet:

| Image may be NSFW. Clik here to view.  |

| Click for larger image |

"Relentless insistence on the idea that . . . the economy will self organize into a state which has satisfactory welfare properties. . . . It has become an assumption." Anyone remotely familiar with mainstream economics knows this is, by any reasonable standard, misleading if not totally false. To the contrary, discovering and describing market failure accounts for a significant portion of economic research. Noah Smith has some nice thoughts on this.

I pointed this out to the tweeter, who responded:

2 approaches:

1. Assume benchmark state is perfect markets and distort your models until they resemble reality.

2. Assume economy is complex and adaptive and watch its history, derive analogies to disequilibrium systems.

Notice the sleight of hand: We started with the claim that the economics profession totally ignores market failure. When I pointed out that the claim is false, we moved to a different complaint: the Rethinkers don't like the way we study market failure. Why not say so in the first place? Click here for another example.

The sleight of hand leaves me with questions about motives. The problem with the critics of macroeconomics is not that macro is perfect as is. It's not. The problem is that they so often start with inaccurate portrayals of what people in the field actually believe and do. Progress in the discipline isn't going to be made this way. Note that this problem exists even within mainstream econ, see e.g. here and here.

Just as politics isn't about policy, perhaps demanding reforms to economics isn't about reforming economics.Image may be NSFW.

Clik here to view.