A lot of people respond to data on declining rates of entrepreneurship by suggesting that this is about the decline of mom-n-pop shops associated with retail sector consolidation. From a recent paper:

If we're just seeing fewer slow growers and likely failures, and if that "small fraction" of young firms that accounts for so much job creation has been unaffected, then less entrepreneurship isn't alarming. Big firms pay better than small firms, and the rise of big box retail has probably made the economy more productive. So Noah Smith and others have pushed back against the growing chorus of declining dynamism alarmism.

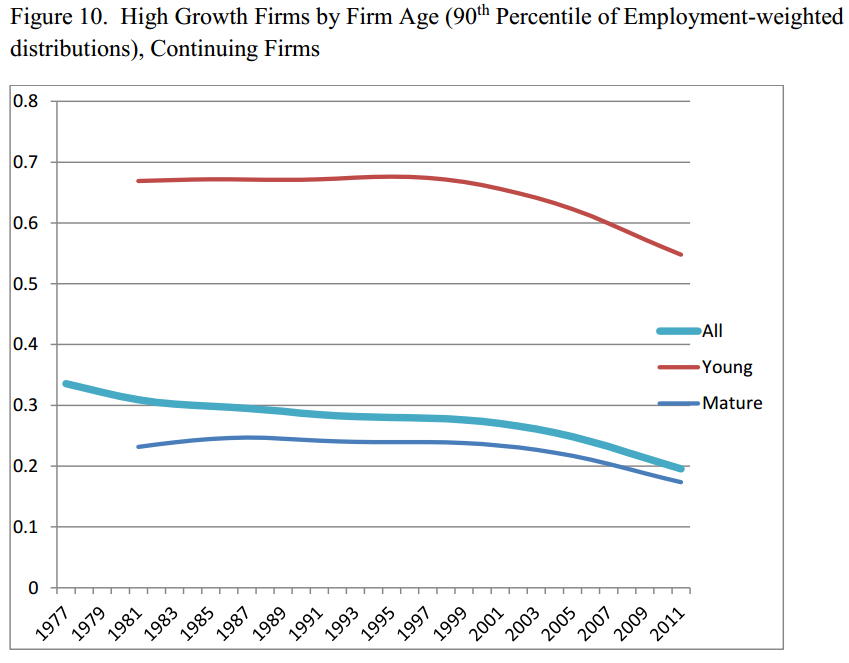

In a preliminary, incomplete working paper, coauthors and I attempt to determine whether the decline of entrepreneurship has involved high-growth firms. One way to do this is to study the distribution of growth rates of young firms (i.e., firms age 5 or less). Figure 10 from that paper is below (click for larger image):

![]()

Most business startups exit within their first ten years, and most surviving young businesses do not grow but remain small. However, a small fraction of young firms exhibit very high growth and contribute substantially to job creation.

If we're just seeing fewer slow growers and likely failures, and if that "small fraction" of young firms that accounts for so much job creation has been unaffected, then less entrepreneurship isn't alarming. Big firms pay better than small firms, and the rise of big box retail has probably made the economy more productive. So Noah Smith and others have pushed back against the growing chorus of declining dynamism alarmism.

In a preliminary, incomplete working paper, coauthors and I attempt to determine whether the decline of entrepreneurship has involved high-growth firms. One way to do this is to study the distribution of growth rates of young firms (i.e., firms age 5 or less). Figure 10 from that paper is below (click for larger image):

|

| Figure from Decker, Haltiwanger, Jarmin, & Miranda (2014) "The secular decline in business dynamism in the U.S." |

The lines indicate the employment-weighted 90th percentile of employment growth rates. That is, only 10 percent of young firm employment is at firms with growth rates that exceed the red line (the series are actually HP filtered). For young firms, the growth rate required to be in the 90th percentile was somewhat constant during the 80s and 90s, suggesting that the decline in entrepreneurship we see in those decades may not have been affecting high-growth firms. But starting around 2000, the top of the growth rate distribution falls. We take this as suggestive evidence that high-growth entrepreneurship began declining around 2000. You can also see that mature firms had a fairly constant distribution before 2000, so that the overall trend was largely a composition effect.

So at least by blog standards I think it's fair to assume that the pre-2000 decline of entrepreneurship may have been largely about the death of the mom-n-pop, but since then even high-growth entrepreneurship has taken a hit. It turns out that the year 2000 is significant for other measures of dynamism, too. The high-tech sector, the information sector, finance, and publicly traded firms all had turning points around that time (see Figure 6 from the working paper), with flat or rising rates of job reallocation and within-firm volatility prior to ~2000 and declining dynamism after ~2000 (and dynamism trends aren't the only thing that changed around 2000; an example). So the story of declining dynamism in the US is partly a story of convergence, with roughly the year 2000 marking a point at which classes of firms that were previously unaffected by the aggregate patterns finally joined the trend.