From the BLS:

I like this data series, with some caveats.* If you're not familiar with this series, note that gross flows are large relative to net flows. Roughly speaking, think of the Great Recession as involving about 8.5 million net job losses. Entering and expanding business establishments create at least half that many jobs even in terrible quarters, but a recession is characterized by even larger numbers of jobs being destroyed by shrinking or closing establishments. So gross flows are large relative to net flows.

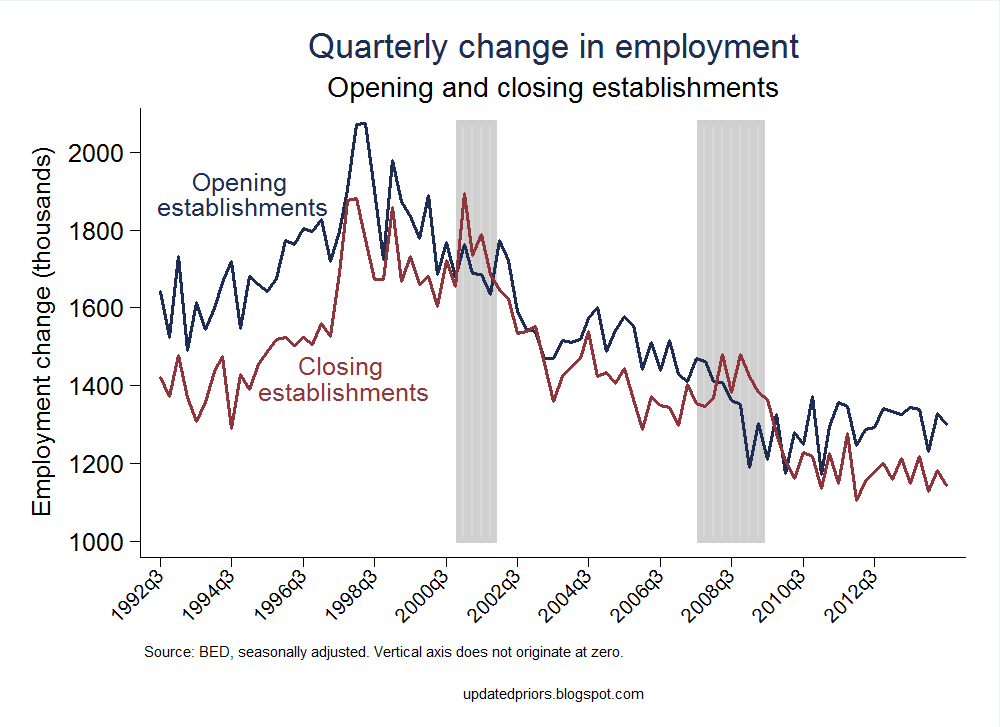

I like to slice the data by extensive margin (opening or closing business establishments) and intensive margin (expanding or contracting existing establishments). Figure 1 reports the flows of employment associated with opening and closing establishments, and Figure 2 reports actual numbers of establishments that opened or closed (click for larger images).

The last time I blogged this series was the 1q2014 release, and that release didn't look great. But, confirming the usual cautions, that release did not seem to mark a new trend. Reallocation from the extensive margin is moving sideways, more or less, with year-over-year job gains from openings slightly down and losses from closings barely changed.

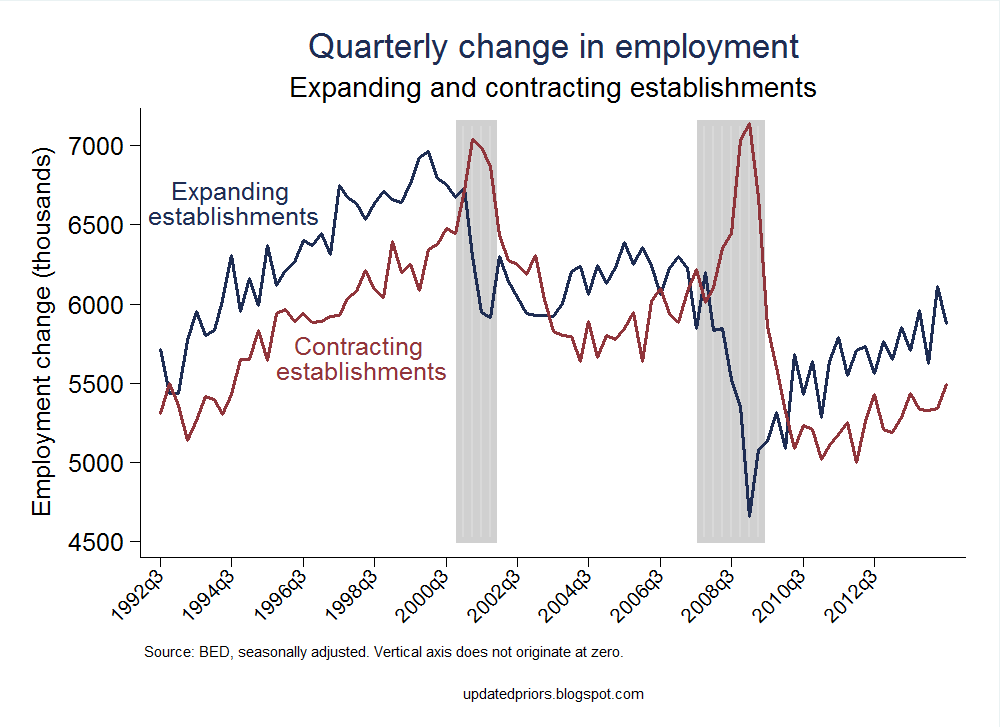

On the intensive margin, reallocation seems to be sticking to its gentle upward trend since the Great Recession. Both jobs created and jobs destroyed on the intensive margin are slightly up year over year.

So there isn't a lot going on along the establishment entry margin, with things pretty much moving sideways (which means fairly constant positive net job creation from entry). Reallocation associated with growth or contraction of existing establishments is steadily rising and may soon approach pre-Great Recession levels.

![]()

From June 2014 to September 2014, gross job gains from opening and expanding private sector establishments were 7.2 million, a decrease of 259,000 jobs from the previous quarter, the U.S. Bureau of Labor Statistics reported today. Over this period, gross job losses from closing and contracting private sector establishments were 6.6 million, an increase of 115,000 jobs from the previous quarter.

I like this data series, with some caveats.* If you're not familiar with this series, note that gross flows are large relative to net flows. Roughly speaking, think of the Great Recession as involving about 8.5 million net job losses. Entering and expanding business establishments create at least half that many jobs even in terrible quarters, but a recession is characterized by even larger numbers of jobs being destroyed by shrinking or closing establishments. So gross flows are large relative to net flows.

I like to slice the data by extensive margin (opening or closing business establishments) and intensive margin (expanding or contracting existing establishments). Figure 1 reports the flows of employment associated with opening and closing establishments, and Figure 2 reports actual numbers of establishments that opened or closed (click for larger images).

|

| Figure 1 |

|

| Figure 2 |

The last time I blogged this series was the 1q2014 release, and that release didn't look great. But, confirming the usual cautions, that release did not seem to mark a new trend. Reallocation from the extensive margin is moving sideways, more or less, with year-over-year job gains from openings slightly down and losses from closings barely changed.

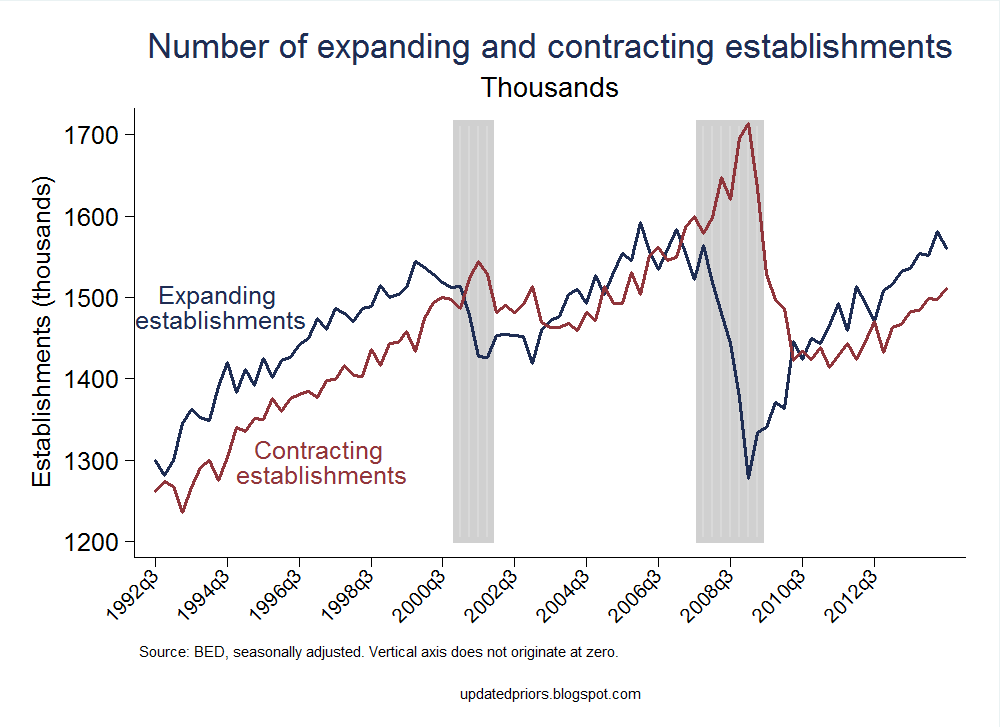

Next, the intensive margin. Figure 3 reports employment flows from expanding and contracting establishments, and Figure 4 reports establishment counts for these categories (click for larger images).

|

| Figure 3 |

|

| Figure 4 |

So there isn't a lot going on along the establishment entry margin, with things pretty much moving sideways (which means fairly constant positive net job creation from entry). Reallocation associated with growth or contraction of existing establishments is steadily rising and may soon approach pre-Great Recession levels.

Now some usual thoughts: gross flows give us an idea of where jobs are being created and destroyed, which fleshes out the net job numbers that are more popular (and timely). More broadly, these data help dissuade us from always thinking in representative agent terms, which is what the net numbers incline people to do. It's tempting to think that net numbers tell us about the experience of most businesses, but in reality there is a lot of heterogeneity among firms, and reallocation proceeds at a high pace.

Some previous BED posts are here.

*The BED are quarterly data provided from the BLS based on state UI data. They are released with a lag of about 8 months. Like the BDS (the dataset I usually use here), the BED basically covers the universe of private nonfarm employers; unlike the BDS, the BED is available at higher frequency and is released more quickly. BED has other drawbacks compared to the BDS, such as a more limited ability to track firms.

The BLS effectively expanded the sample definition in the first quarter of 2013. The 2013q1 observation was the most obviously affected, as it reported all establishments that were added to the sample as establishment openings. For openings data, I have replaced the 2013q1 observation with the average of 2012q4 and 2013q2. I haven't dug into the data enough to know whether users can manually correct for this over the longer run.

It is also important to note that these numbers are seasonally adjusted, and any guess at net numbers based on the difference between two seasonally adjusted series is very, very rough. Non-SA numbers are available on the BLS website.

These numbers track business establishments, which are different from firms. Costco is a firm; your local Costco store is an establishment. Most firms consist of only one establishment. The BED is not ideal for tracking firms, as it has limited ability to correctly link establishments to the firm level.